How to buy a house with $0 down in 2021: First time buyer

No-down-payment mortgage

A no-down-payment mortgage allows first-time home buyers and repeat home buyers to purchase property with no money required at closing, except standard closing costs.

Other options, including the FHA loan, the HomeReady mortgage, and the Conventional 97 loan, offer low down payment options with a little as 3% down. Mortgage insurance premiums typically accompany low and no down payment mortgages, but not always.

Is a no-down-payment mortgage right for you?

It’s a terrific time to buy a home.

Sales are rising, supply is dropping, and prices have increased in many cities and neighborhoods. Compared to next year, today’s market may look like a bargain.

Furthermore, mortgage rates are still low.

Rates for 30-year loans, 15-year loans, and 5-year ARMs are historically cheap, which has lowered the monthly cost of owning a home.

No down payment: USDA loans (100% financing)

The U.S. Department of Agriculture offers a 100% financing mortgage. The program is formally known as a Section 502 mortgage, but, more commonly, it’s called a ’Rural Housing Loan’ or simply a ’USDA loan.’

The good news about the USDA Rural Housing Loan is that it’s not just a “rural loan“ — it’s available to buyers in suburban neighborhoods, too. The USDA’s goal is to help “low-to-moderate income homebuyers,“ wherever they may be.

Many borrowers using the USDA loan program make a good living and reside in neighborhoods that don’t meet the traditional definition of a ’rural area.’

For example, college towns including Christiansburg, Virginia; State College, Pennsylvania; and even suburbs of Columbus, Ohio meet USDA eligibility standards. So do the less-populated suburbs of some major U.S. cities.

Some key benefits of the USDA loan are :

- There’s no down payment requirement

- There’s no maximum home purchase price

- You may include eligible home repairs and improvements in your loan amount

- The upfront guarantee fee can be added to the loan balance at closing; mortgage insurance is collected monthly

Just be aware that USDA enforces income limits; yours must be near or below the median income for your area .

Another key benefit is that USDA mortgage rates are often lower than rates for comparable, low- or no-down-payment mortgages. Financing a home via the USDA can be the lowest-cost path to homeownership.

Low down payment: FHA loans (3.5% down)

The ’FHA mortgage’ is a bit of a misnomer because the Federal Housing Administration (FHA) doesn’t actually lend money. Rather, the FHA is an insurer of loans.

The FHA publishes a series of standards for the loans it will insure. When a borrower meets these specific guidelines, the FHA agrees to insure that loan against loss.

FHA mortgage guidelines are famous for their liberal approach to credit scores and down payments.

The FHA will typically insure home loans for borrowers with low credit scores, so long as there’s a reasonable explanation for the low FICO.

The FHA allows a down payment of just 3.5% in all U.S. markets, with the exception of a few FHA approved condos .

Other benefits of an FHA loan are :

- Your down payment may come entirely from gift funds or down payment assistance

- The minimum credit score is 500 with a 10% down payment, or 580 with a 3.5% down payment

- Upfront mortgage insurance premiums can be included in the loan amount; mortgage insurance is paid monthly thereafter

Furthermore, the FHA can sometimes help homeowners who have experienced recent short sales, foreclosures, or bankruptcies.

The FHA insures loan sizes up to $822375 in designated “high-cost“ areas nationwide. High-cost areas include places like Orange County, California; the Washington D.C. metro area; and, New York City’s 5 boroughs.

Note that if you want to use an FHA loan, the home being purchased must be your primary residence. This program isn’t intended for vacation homes or investment properties.

Low down payment: The HomeReady Mortgage (3% down)

The HomeReady mortgage is special among today’s low- and no-downpayment mortgages.

Backed by Fannie Mae and available from nearly every U.S. lender, the HomeReady mortgage offers below-market mortgage rates, reduced mortgage insurance costs, and the most innovative underwriting in more than a decade.

Via HomeReady, the income of everybody living in the home can be used to get mortgage-qualified and approved.

For example, if you are a homeowner living with your parents, and your parents earn an income, you can use their income to help you qualify.

Similarly, if you have children who work and contribute to household expenses, those incomes can be used for qualification purposes, too.

The HomeReady program also lets you use boarder income to help qualify, and you can use income from a non-zoned rental unit, too — even if you’re paid in cash.

HomeReady home loans were designed to help multi-generational households get approved for mortgage financing. However, the program can be used by anyone in a qualifying area, or who meets household income requirements.

Low down payment: Conventional loan 97 (3% down)

The Conventional 97 program is available from Fannie Mae and Freddie Mac. It’s a 3% down payment program and, for many home buyers, it’s a less expensive loan option than an FHA mortgage.

The Conventional 97 basic qualification standards are :

- Loan size may not exceed $548250, even if the home is in a high-cost market

- The property must be a single-unit dwelling. No multi-unit homes are allowed

- The mortgage must be a fixed-rate mortgage. No ARMs are allowed via the Conventional 97

The Conventional 97 program does not enforce a specific minimum credit score beyond those for a typical conventional home loan. The program can be used to refinance a home loan, too.

In addition, the Conventional 97 mortgage allows for the entire 3% down payment to come from gifted funds, so long as the gifter is related by blood or marriage, legal guardianship, domestic partnership, or is a fiance/fiancee.

No down payment: VA loans (100% financing)

No down payment: VA loans (100% financing)

The VA loan is a no-money-down program available to members of the U.S. military and surviving spouses.

Backed by the U.S. Department of Veterans Affairs, VA loans are similar to FHA loans in that the agency guarantees loans for borrowers who meet VA mortgage guidelines.

VA loan qualifications are straightforward.

Most veterans, active duty, and honorably discharged service personnel are eligible for the VA program. In addition, home buyers who have spent at least 6 years in the Reserves or National Guard are eligible, as are spouses of service members killed in the line of duty.

Some key benefits of the VA loan are :

- No down payment requirement

- Flexible credit score minimums

- Below-market mortgage rates

- Bankruptcy and other derogatory credit information does not immediately disqualify you

- No mortgage insurance is required, only a one-time funding fee which can be included in the loan amount

In addition, VA loans have no maximum loan amount. It’s possible to get a VA loan above current conforming loan limits, as long as you have strong enough credit and you can afford the payments.

The “ piggyback loan “ or “80/10/10“ program is typically reserved for buyers with above-average credit scores. It’s actually two loans, meant to give home buyers added flexibility and lower overall payments.

The beauty of the 80/10/10 is its structure.

With an 80/10/10 loan, buyers bring a 10% down payment to closing. This leaves 90% of the home sale price for the mortgage.

But, instead of getting one mortgage for 90%, the buyer splits the loan into two parts.

The first part of the 80/10/10 is the “80.“

The “80“ represents the first mortgage and is a loan for 80% of the home’s purchase price. This is typically a conventional loan via Fannie Mae or Freddie Mac, and it’s offered at current market mortgage rates.

The first “10“ represents a second mortgage. This is a loan for 10% of the home’s purchase price. This loan is typically a home equity loan (HELOAN) or home equity line of credit (HELOC).

Home equity loans are fixed-rate loans. Home equity lines of credit are adjustable-rate loans. Buyers can choose from either option. HELOCs are more common because of the flexibility they offer over the long-term.

And that leaves the last “10,“ which represents the buyer’s down payment amount — 10% of the purchase price. This amount is paid as cash at closing.

80/10/10 loans are sometimes called piggyback loans because the second mortgage “piggybacks“ on the first one to increase the total amount borrowed.

80/10/10 loans are meant to give buyers access to the best pricing available, so lenders may sometimes recommend an alternate structure. For example, if you’re buying a condo, a 75/15/10 structure is advised because condo mortgages get better rates with LTVs of 75% or less.

As another example, interest rates on HELOCs are sometimes better at larger loan sizes. Your lender may recommend that you increase the size of your HELOC to lower your overall loan costs.

Ultimately, though, you get to choose your loan’s structure. You can’t be forced into borrowing more money on your second mortgage than makes you comfortable.

Home buyers don’t need to put 20% down

It’s a common misconception that “20 percent down“ is required to buy a home. And, while that may have true at some point in history, it hasn’t been so since the advent of the FHA loan in 1934.

In today’s real estate market, home buyers don’t need to make a 20% down payment. Many believe that they do, however ( despite the obvious risks ).

The likely reason buyers believe 20% down is required is because, without 20% down, you’ll likely have to pay for mortgage insurance. But that’s not necessarily a bad thing.

PMI is not evil

Private mortgage insurance (PMI) is neither good nor bad , but many home buyers still try to avoid it at all costs.

The purpose of private mortgage insurance is to protect the lender in the event of foreclosure — that’s all it’s for. However, because it costs homeowners money, PMI gets a bad rap.

It shouldn’t.

Because of private mortgage insurance, home buyers can get mortgage-approved with less than 20% down. And, eventually, private mortgage insurance can be removed.

At the rate today’s home values are increasing, a buyer putting 3% down might pay PMI for fewer than four years.

That’s not long at all. Yet many buyers — especially first-timers — will put off a purchase because they want to save up 20 percent.

Meanwhile, home values are climbing.

For today’s home buyers, the size of the down payment shouldn’t be the only consideration.

This is because home affordability is not about the size of your down payment — it’s about whether you can manage the monthly payments and still have cash left over for “life.“

A large down payment will lower your loan amount, and therefore will give you a smaller monthly mortgage payment. However, if you’ve depleted your life savings in order to make that large down payment, you’ve put yourself at risk.

Don’t deplete your entire savings

When the majority of your money is tied up in a home, financial experts refer to it as being “house-poor.“

When you’re house-poor, you have plenty of money “on-paper,“ but little cash available for the everyday living expenses and emergencies.

And, as every homeowner will tell you, emergencies happen.

Roofs collapse, water heaters break, you become ill and cannot work. Insurance can help you with these issues sometimes, but not always.

That’s why you being house-poor can be so dangerous.

Many people believe it’s financially conservative to put 20% down on a home. If 20% is all the savings you have, though, using the full amount for a down payment is the opposite of being financially conservative.

The true financially conservative option is to make a small down payment and leave yourself with some money in the bank. Being house-poor is no way to live.

Mortgage down payment FAQ

Mortgage down payment FAQ

Here are answers to some of the most frequently asked questions about mortgage down payments.

How can I buy a house with no money down?

In order to buy a house with no money down, you’ll just need to apply for no-money-down mortgage. If you don’t know which mortgage loan is your best zero money down option, that’s okay. A mortgage lender can help steer you in the right direction. There are multiple 100 percent mortgages available for today’s home buyers.

Can cash gifts be used as a down payment?

Yes, cash gifts can be used for a down payment on a home. However, when you’re receiving a cash gift, you’ll want to make sure you follow a few procedures.

For example, make sure the gift is made using a personal check, a cashier’s check, or a wire; and keep paper records of the gift, including photocopies of the checks and of your deposit to the bank. Also, make sure your deposit matches the amount of the gift exactly.

Your lender will also want to verify that the gift is actually a gift and not a loan in disguise. Cash gifts do not require repayment.

What are down payment assistance programs?

Down payment assistance programs are available to home buyers nationwide, and 87% of U.S. single-family homes potentially qualify. Programs will vary by state, so be sure to ask your mortgage lender which programs you may be eligible for. The average home buyer using down payment assistance receives $11,565.

Are there any home buyer grants?

Home buyer grants are offered in every state, and all U.S. home buyers can apply. These are also known as down payment assistance (DPA) programs. DPA programs are widely available but seldom used — 87% of single-family homes potentially qualify, but less than 10% of buyers think to apply. Your mortgage lender can help you determine which DPAs are best for you.

What are FHA loan requirements?

FHA loan requirements are: 1) You must have a credit score of at least 500; 2) Your income can be verified using W-2 statements and paystubs, or federal tax returns; 3) You have no history of bankruptcy, foreclosure, or short sale within the last 12 months; 4) You must not be delinquent on your federal taxes, your federal student loans, or any other federal debt; 5) The home being purchased must be a primary residence and not exceed local FHA loan limits.

What are the benefits to putting more money down?

Just as there are benefits to low- and no-money-down mortgages, there are benefits to putting more money down on a purchase. For example, when you put more money down on a home, the amount you need to mortgage is less, which reduces your monthly mortgage payment. Additionally, if your loan requires mortgage insurance, with more money down, your mortgage insurance will “cancel“ in fewer years.

If I make a low down payment, do I pay mortgage insurance?

When you make a low down payment, you’re more likely to pay mortgage insurance (MI), but not necessarily. For example, the VA Home Loan Guaranty program doesn’t require mortgage insurance, so if you use a VA loan, making a low downpayment won’t matter. Conversely, FHA and USDA loans always require mortgage insurance so even with large down payments, you’ll have a monthly MI charge.

The only loan for which your down payment affects your mortgage insurance is the conventional mortgage. The smaller your down payment, the higher your monthly PMI. However, once your home has 20% equity, you’ll be eligible to have your PMI removed.

If I make a low down payment, what are my lender fees?

The size of your down payment doesn’t relate to your lender fees. No matter how large or how small your down payment, your lender fees should remain equal. This is because mortgage lenders are prohibited from charging higher fees based on the size of your down payment. It should be noted, however, that different loan types may require different services (e.g.; home inspection, roof inspection, home appraisal), and this may affect your total loan closing costs.

What is the minimum down payment for a mortgage?

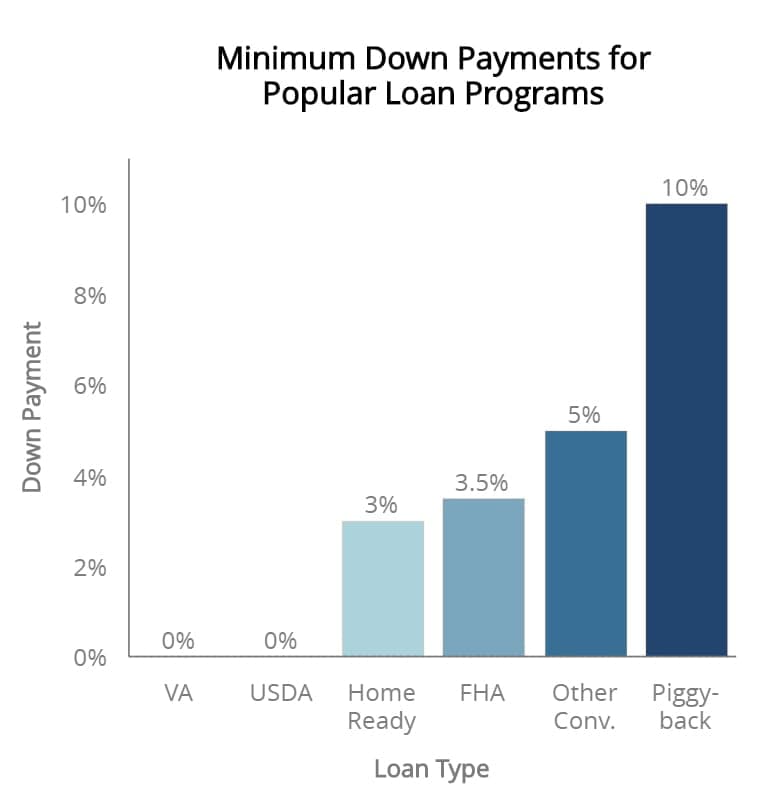

The minimum down payments by mortgage program are: VA loan: 0% down payment; USDA loan: 0% down payment; Conventional 97 mortgage: 3% down payment; HomeReady mortgage: 3% down payment; and FHA loan: 3.5% down payment. In addition to these programs, down payment assistance programs are often available and provide, on average, more than $11,000 to today’s home buyers.

Are there zero down mortgage loans?

Zero-down mortgages are 100% financed loan types offered by the U.S. Department of Agriculture (USDA loan or “Rural Housing Loan“) and the Department of Veteran Affairs (VA loan). Additionally, there are several low down payment options like the FHA loan (3.5% down), the conventional 97% (3% down,) and the HomeReady or Home Possible mortgage (3% down).

How can I fund a down payment?

A down payment can be funded in multiple ways, and lenders are often flexible. Some of the more common ways to fund a down payment are to use your savings or checking account, or, for repeat buyers, the proceeds from the sale of your existing home.

However, there are other ways to fund a down payment, too.

For example, home buyers can receive a cash gift for their down payment or can borrow from their 401k or IRA ( although that’s not always wise ).

Down payment assistance programs can fund a down payment, too. Typically, down payment assistance programs loan or grant money to home buyers with the stipulation that they live in the home for a certain number of years — often 5 years or fewer.

Regardless of how you fund your down payment, make sure to keep a paper trail. Without a clear account of the source of your down payment, a mortgage lender may not allow its use.

How much home can I afford?

The answer to the question of “How much home can I afford?“ is a personal one, and should not be left solely to your mortgage lender.

The best way to answer the question of how much can you afford for a home is to start with your monthly budget and determine what you can comfortably pay for a home each month.

Then, using your desired payment as the starting point, use a mortgage calculator and work backward to find your maximum home purchase price.

Note that today’s mortgage rates will affect your mortgage calculations, so be sure to use current mortgage rates in your estimate. When mortgage rates change, so does home affordability.

What are today’s low-down-payment mortgage rates?

Today’s mortgage rates are low across the board. And many low-down-payment mortgages have below-market rates thanks to their government backing; this includes FHA loans (3.5% down) and VA and USDA loans (0% down).

Different lenders offer different rates, so you’ll want to compare a few mortgage offers to find the best deal on your low- or no-down-payment mortgage. You can get started right here.

Source: https://themortgagereports.com/

…Let us join your journey of getting your dream house!

Call now:(617) 201-9188 Ana Roque |209 West Central Street, Natick, MA

Ana Roque is a Brazilian Licensed Realtor at Re-Connect, LLC with 16+ years of experience in the Real Estate industry.

Ana Roque is a Brazilian Licensed Realtor at Re-Connect, LLC with 16+ years of experience in the Real Estate industry.

Ana speaks 3 languages (Portuguese, English, Spanish), Wife, Stepmom, Journalist, Event Director for the National Association of Hispanic Real Estate Professionals (NAHREP) Central MA Chapter.

Ana is a self-motivated, goal-orientated and focused on building her career with partners and develop leadership with excellence to her teamwork as a mission to create a legacy to her clients and children.

WHAT WE OFFER

Buyer’s agent | Listing agent | Short-Sale | Foreclosure | Rehab homes | Commercial R.E.

![]()

How to Get Pre-Approved for a Mortgage in Massachusetts If you're planning to buy a home in Massachusetts, one of the smartest first steps is getting pre-approved for a mortgage. In today's competitive real estate market, sellers often favor buyers who already have financing lined Read more

FHA vs Conventional Loans: Which Is Better in Massachusetts? Buying a home is one of the biggest financial decisions you'll ever make, and choosing the right mortgage is just as important as finding the perfect property. If you're planning to purchase a home in Massachusetts, Read more

What Is Fix and Flip? A Complete Guide to Flipping Houses and Its Benefits Fix and flip is a real estate investment strategy where an investor purchases a property that needs repairs or renovations, improves it, and then sells it for a profit. Rather than Read more

5 Home Improvements That Increase Property Value If you're planning to sell your home, making the right improvements before listing it can help you attract more buyers, sell faster, and maximize your return on investment (ROI). However, not every renovation adds significant value. Some projects Read more