6 reasons to refinance your mortgage. If you’re a homeowner, you might be hearing everyone—from your neighbors to news anchors—talking about refinancing. So, should you be considering it too? There are many situations in which refinancing your mortgage may be right for you. Let’s go over some of the major reasons:

What is refinancing a mortgage?

What is refinancing a mortgage?

When you refinance your mortgage, you are basically swapping out your old loan for a new one. There are two main types of refinances:

Rate-and-term refinance:

The remaining balance on your current mortgage is transformed into a new loan that has a better rate and/or term for your situation.

Cash-out refinance:

You liquidate some of your home’s equity, creating a new loan that consists of your previous mortgage balance plus the cash you took out.

You can get a refinance from any mortgage lender you choose—it doesn’t have to be from your current lender. We encourage you to shop around when refinancing, just like you (hopefully) did when you first got your mortgage.

Reasons to refinance your mortgage

So, why might you consider refinancing in the first place? It all depends on your goals. People choose to refinance for a number of reasons, but here are some of the most common motivators:

1. You want to lower your monthly payments

If rates have dropped since you got your original mortgage, you may be able to refinance into a loan with a lower rate. Doing so may lower your monthly payments, meaning you may also pay less over the life of your loan. To find out if you stand to save on your monthly payments, you can check today’s rates in seconds.

Alternatively, if rates haven’t dropped significantly but you have had or anticipate a decrease in income, you may be able to lengthen your loan term to pay off your loan more gradually. For example, if you switch from a 15-year fixed-rate mortgage into a 30-year fixed-rate mortgage, you can make lower monthly payments. However, it’s important to note that you’ll also have to pay interest for a longer period of time.

Finally, if you’ve paid off a significant amount of your mortgage or your home’s value has increased, then your loan-to-value ratio (LTV) will be smaller. A smaller loan amount compared to the value of your home means that the loan is considered lower risk to the lender—which can help you get a better rate. If you’ve recently passed the 20% mark for equity in your home and you’ve been paying for private mortgage insurance, you can also refinance to cancel your mortgage insurance.

2. Your credit score has improved

If your credit score has gotten a significant boost, you may also be able to refinance to get a better rate. For example, depending on the specifics of the loan, a 20-point increase in your credit score could reduce your rate enough to help you save thousands of dollars in interest over the life of the loan.

Paying bills on time, paying down debts, and lowering your overall credit utilization are a few ways you can improve your credit score. It’s a good idea to regularly monitor your credit score so you have a good idea of where it stands and when you might have enough leverage to refinance for a lower rate.

3. The fixed period on your adjustable-rate mortgage is ending

While adjustable-rate mortgages (ARMs) can save you money on your monthly mortgage payment in the early years of owning a home, once the fixed period ends, your interest rate may increase quite a bit. You can avoid this by switching from an ARM to a fixed-rate mortgage. While your new fixed rate will likely be higher than your original adjustable rate, you’ll be protected from future rate increases. (On the flipside, if you know you’ll be selling your house in the next few years, switching to an adjustable-rate mortgage could lower your rate and monthly payments until the fixed period ends and/or you sell your house.)

4. You can afford higher monthly payments

In some cases, changing the length of your loan when refinancing can be advantageous. If you can afford higher monthly payments, thanks to an increase in income, you could refinance into a shorter loan (such as from a 30-year fixed-rate mortgage to a 15-year fixed-rate mortgage) to pay it off faster, saving thousands of dollars in interest payments over the life of the loan.

5. You want to take cash out

You can also do a cash-out refinance, which allows you to use the equity you’ve built in your home to borrow money. Homeowners often reinvest that cash out back into their home to make renovations or repairs that boost their home’s value. Taking cash out can also be useful if you need extra money for expenses such as education or medical costs and don’t have access to other funds.

So, how exactly does a cash-out refinance work? Let’s say your home is worth $300,000 and you have $100,000 left on your current mortgage. That means you have $200,000 in home equity that you can borrow against. In this instance, you could choose to do a cash-out refinance for $30,000 of your equity and your new mortgage would be for $130,000.

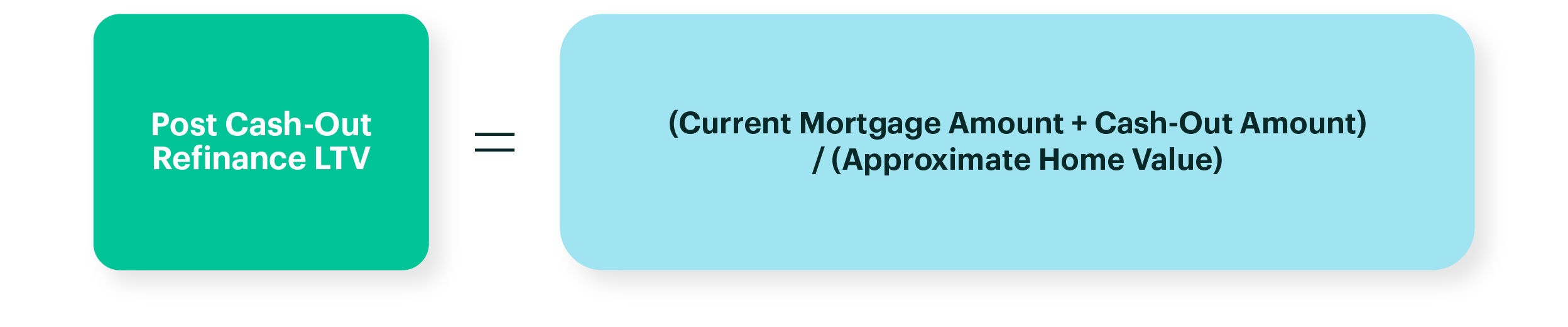

Since lenders view cash-out refinances as riskier than rate-and-term refinances, interest rates are generally higher. However, you may still be able to get a better interest rate than your current financing, particularly if rates have dropped or your credit score has improved since you got your original mortgage. To be eligible for a cash-out refinance, most lenders also require that your loan-to-value ratio (LTV) stays at or below 80% post-refinance (for a single-unit primary residence; maximum LTVs for other properties may vary). You can calculate your cash-out refinance LTV using this simple equation:

6. You want to consolidate debt

Finally, you can refinance to consolidate other debts into a single, more affordable payment. This may be especially helpful if you have high-interest loans and debts like credit card debt, student loans, or a second mortgage. A debt consolidation refinance is technically considered a cash-out refinance, so they work in a similar way. Essentially, a portion of your home equity is turned into cash that you can use to pay off other loans and debts. Your old mortgage will be replaced by a new one that includes the amount you took out to pay those other debts.

Consolidating credit card debt in this way can especially be advantageous because of the difference in credit card and mortgage interest rates. As of May 2020, the average credit card interest rate in the U.S. is 14.52%. At the same time, mortgage rates are hitting historic lows. By moving your credit card debt to your mortgage, you may be able to save a significant amount from the lower interest rate in the long term. Mortgage interest is also usually tax-deductible, unlike credit card interest, offering another opportunity to save money by consolidating.

Is refinancing a good idea for you?

While there can be many benefits to refinancing, it’s important to remember that you’ll still have to complete a loan application and pay closing costs, similar to the ones you paid when you got your original mortgage. You’ll likely have to pay things like lender fees, appraisal fees, and title insurance fees.

If you’re looking to get a better rate or term by refinancing, you should consider the break-even point: the length of time it will take for you to recoup the costs of refinancing. If you expect to remain in your current home beyond the break-even point, then it may be a good idea to refinance your mortgage. Otherwise, the upfront costs of refinancing won’t outweigh the potential long-term savings.

If you only plan to keep the home for a few more years, you may want to consider what’s called a “no-cost” refinance, where you offset your closing costs by raising your refinance rate (i.e. taking credits). For a cash-out or debt consolidation refinance, you should also compare the benefit of how you’ll be using the money you take from your equity against the added time (and interest) it may take to pay off the loan.

Source: https://better.com/ | By Lucy Randall (NMLS ID: 1571868)

Are you ready to take the next step to buy your home and start building a legacy for your family?…Let me help you!

I am a Brazilian Licensed Realtor at Re-Connect, LLC with 17+ years of experience in the Real Estate industry. I speaks 3 languages (Portuguese, English, Spanish)

CALL NOW: (617) 201-9188 Ana Roque |209 West Central Street, Natick, MA

![]()

![]()